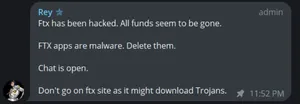

An FTX account administrator wrote on the FTX support Telegram, "FTX has been hacked. FTX apps are malware. Delete them. Chat is open. Don't go on FTX site as it might download Trojans". The message was pinned by FTX General Counsel Ryne Miller.

Miller later wrote on Twitter, "Investigating abnormalities with wallet movements related to consolidation of ftx balances across exchanges - unclear facts as other movements not clear. Will share more info as soon as we have it."

A Telegram admin subsequently wrote, "Not all hope is lost. Engineers have managed to retrieve substantial amount of funds," but no details were provided beyond that. A later announcement by Miller claimed that FTX had "initiated precautionary steps to move all digital assets to cold storage", suggesting some of the transfers may have been a part of that effort.

Many speculated that the so-called hack had been coordinated by insiders.