The idea was to use a private blockchain to "promote more efficient and secure global trade" by allowing shipping companies to share information including shipping container contents and tracking. However, it was apparently tough to convince these companies to actually adopt the project, and Maersk and IBM pulled the plug.

Maersk and IBM announce the discontinuation of their blockchain-based TradeLens platform

Tough news for folks who insist that blockchains' obvious use case is for supply chains: IBM and Maersk have discontinued their private blockchain-based TradeLens platform due to lack of interest.

Auros misses loan payment due to FTX exposure

Crypto trading firm Auros missed a payment on its 2,400 wETH (~$3 million) loan from the Maple defi lending project. According to M11 Credit, the operator of the credit pool from which Auros has taken the loan, this was due to "a short-term liquidity issue as a result of the FTX insolvency".

In total, Auros has 8,400 wETH (~$10.7 million) and $7.5 million in USDC in loans from M11 credit pools, plus another $2.4 million in loans from the Clearpool defi lending project, for a total of more than $20 million in unsecured loans.

Kraken pays over $360,000 to settle violations of sanctions against Iran

The US cryptocurrency exchange Kraken settled charges from the Office of Foreign Assets Control (OFAC) alleging that they had violated sanctions against Iran. In the agreement, Kraken will pay $362,158.70 for the potential civil liability, and agree to commit $100,000 in various compliance controls.

The OFAC investigation was first revealed in July, in reporting from the New York Times.

- Settlement Agreement between the U.S. Department of the Treasury’s Office of Foreign Assets Control and Payward, Inc. ("Kraken"), U.S. Department of the Treasury

Kraken lays off 1,100 employees in 30% cut

The US cryptocurrency exchange Kraken announced that it had laid off 30% of its employees, or about 1,100 people. They blamed "macroeconomic and geopolitical factors" resulting in less trading and fewer clients. "Unfortunately, negative influences on the financial markets have continued and we have exhausted preferable options for bringing costs in line with demand," they wrote.

Bitso lays off more employees

After cutting around 10% of their employees in May, the Latin American crypto exchange Bitso has performed another round of layoffs.

The company didn't reveal how many employees were affected by the layoffs, but Portal do Bitcoin estimated that around 100 employees were let go — around 15–20% of the company's remaining staff. One employee wrote on LinkedIn that he was among "dozens" who were laid off.

- "Bitso cuts more staff in fresh round of layoffs", The Block

- "Corretora de criptomoedas Bitso faz segunda rodada de demissões no Brasil e no México", Portal do Bitcoin (in Portuguese)

Block subsidiary TBD announces they will trademark "Web5", cancels plans after completely foreseeable backlash

TBD is a subsidiary of Block (formerly Square), a tech company co-founded by billionaire social media mogul and Twitter founder Jack Dorsey. In July, they unveiled the concept of "Web5", which they define an "extra decentralized web platform".

Who could have predicted that people might balk when TBD then announced they would try to trademark the term? Apparently they saw no irony in their attempt as a single, powerful entity to gain control over the trademark.

The same was not true of the people who responded to the post, who wrote things like, "We need to make sure web 5 is truly open by copyrighting it", and simply "🤡🤡🤡🤡🤡".

Six hours later, the company tweeted, "we have heard the community and we are responding to their concerns". They issued a statement acknowledging that "we have heard loud voices in the community who are concerned about the potential for abuse of trademark law in ways that would undermine the mission of decentralization." Gee, you think?

And no, they still haven't explained what happened to web4.

BlockFi files for bankruptcy

Crypto lending firm BlockFi has filed for Chapter 11 bankruptcy in the wake of the FTX collapse. The company was in dire straits in the spring after Terra and Three Arrows Capital blow-ups, but was bailed out in June by a $250 million loan from FTX, followed by a deal giving BlockFi a $400 million credit facility and giving FTX the "option to acquire" BlockFi.

Because of this dependency, it was no surprise when BlockFi announced they were once again in crisis following the FTX explosion. On November 15, the Wall Street Journal reported they were preparing for possible bankruptcy and considering layoffs.

On November 28, BlockFi filed for bankruptcy. Their filing estimates they have more than 100,000 creditors (the maximum option on the form), between $1–10 billion in assets, and between $1–10 billion in liabilities.

Shitcoin project tests the limits of cringe by building $600,000 statue of Elon Musk and delivering it to Tesla HQ

A shitcoin project desperate for the kind of pump that sometimes occurs when Elon Musk tweets about a cryptocurrency has gone to new lengths to get his attention. The group spent $600,000 and six months on a six-ton statue that's supposed to be Elon Musk's head on a rocket ship, but looks rather like a giant Elon Musk caterpillar.

The group then delivered the sculpture to Tesla HQ in Austin, Texas, and is reportedly refusing to leave until he accepts the statue. Unfortunately he may be too busy burning Twitter to the ground to have noticed.

Despite receiving press coverage in outlets including the Wall Street Journal, Fox Business, and USA Today, the project has as of yet failed to achieve much of a pump, and the token is trading around where it was several months ago. I've not named the token here in the hopes of not contributing to the goals of their viral marketing stunt.

150 companies seek Binance's bailout for organizations "facing significant, short term, financial difficulties"

On November 14, CZ of Binance announced an "industry recovery fund", which he said would devote money to ending "further cascading negative effects of FTX [and] help projects who are otherwise strong, but in a liquidity crisis".

In a blog post outlining the $1 billion initiative, Binance also divulged that "we have already received around 150 applications from companies seeking support under the [Industry Recovery Initiative]" — only a week and a half after it was announced.

Lemon Cash crypto exchange lays off almost 40% of its staff

The Argentinean cryptocurrency exchange Lemon Cash announced that they had laid off 38% of their employees, or around 100 people. The CEO blamed the international crypto environment, as well as a "recessionary period" in startup investments. He also urged that the announcement was not related to the FTX collapse, and explained that although the company had user funds stored with FTX, they withdrew them prior to FTX halting withdrawals.

Lemon had closed a $44.1 million series A funding round earlier this year, which they kicked off in July 2021.

- "Carta abierta a la comunidad" ["Open letter to the community"], Lemon Cash blog (in Spanish)

Users unable to withdraw from CoinList due to protracted "technical difficulties"

Beginning in mid-November, users of the CoinList exchange and ICO platform reported that they couldn't withdraw assets from the platform. On November 24, CoinList tweeted, "There is a lot of FUD going around that we would like to address head on. CoinList is not insolvent, illiquid, or near bankruptcy. We are experiencing technical issues that are affecting deposits and withdrawals." This was not entirely reassuring, given the number of companies in the crypto industry who have announced they were just fine before being revealed to be deeply underwater.

CoinList lost $35 million in the June Three Arrows blowup. Shortly after the FTX collapse, CoinList claimed to have "no material exposure to FTX, FTT, Alameda or any credit exposure to any affiliate of FTX". However, they stopped processing withdrawals shortly after.

Iris Energy defaults on $100 million+ loan, unplugs miners

After announcing earlier in the month that they were close to defaulting on a $100 million+ loan, Iris Energy has defaulted. Unable to pay the $7 million/month in debt obligations with their $2 million/month gross profit, Iris Energy has powered off 3.6 EH/s worth of mining capacity.

Iris Energy's stock has plummeted to $1.66, down 93% from its $24.80 peak when the stock first began trading a year ago.

New York institutes two-year ban on new crypto-mining operations at fossil fuel plants

Governor Kathy Hochul signed legislation to ban for two years the issuance of permits to new crypto-mining operations at fossil fuel plants. This seeks to cut down on the enormous energy costs of proof-of-work crypto-mining used for cryptocurrencies such as Bitcoin.

New York has been the home of some battles against crypto-miners who have set up shop at dormant fossil fuel plants. The Greenidge Bitcoin mining operation near Seneca Lake has been the locus of some particularly bitter battles against the industry: a dormant coal power plant that was converted to natural gas and devoted to Bitcoin mining in 2019, its permit renewals have been the focus of fierce protests. It will not be affected by this particular legislation, which only bans mining operations who have not already submitted applications for new or renewed permits.

- "New York Enacts 2-Year Ban on Some Crypto-Mining Operations", The New York Times

Genesis warns of bankruptcy if it can't raise $1 billion

Genesis Global Trading has reportedly been telling investors that Genesis may need to file for bankruptcy if its attempts to raise at least $1 billion in new capital don't succeed. The firm revealed its exposure to FTX last week, halting withdrawals from its lending service and acknowledging that its derivatives arm has $175 million in funds locked in the bankrupt exchange.

The Wall Street Journal then reported that Genesis had been seeking a $1 billion emergency loan due to a "liquidity crunch due to certain illiquid assets on its balance sheet".

The halting of withdrawals from Genesis' lending business has already had major downstream impacts, as it is a major partner of other crypto lending services. Gemini and Coinhouse both followed Genesis in suspending withdrawals, as did other firms including Donut and GOPAX.

A Genesis bankruptcy would be a monumental event in crypto, with enormous downstream exposure.

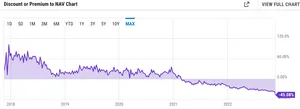

Grayscale Bitcoin Trust suffers due to FTX collapse and doubts over reserves

Grayscale Bitcoin Trust (GBTC), the largest publicly traded crypto fund, hit record lows in the wake of the FTX collapse. The fund was trading at nearly a 50% discount on the underlying Bitcoin asset, as holders rushed to sell off their GBTC holdings.

This was not helped by Grayscale's response to those in crypto who were pushing Grayscale to follow suit with some other crypto platforms and publish proof of reserves. Grayscale announced that "due to security concerns, we do not make such on-chain wallet information and confirmation information publicly available through a cryptographic Proof-of-Reserve, or other advanced cryptographic accounting procedure". They did not elaborate on what these "security concerns" might be, and stoked fears in some that the company might not have the backing they ought to have.

Grayscale published a letter from Coinbase that basically said "we have Grayscale's assets, we promise", which did not seem to assuage the fears that have formed around centralized entities promising they have the assets they claim. This is understandable, given that FTX made similar promises, only to collapse.

Hoo Exchange vanishes

On June 19, the Hong Kong-based crypto exchange Hoo announced that they would be pausing withdrawals for "24–72 hours" while they transferred some assets to top up their hot wallet.

Since then, there has been little communication and a series of shady activities. According to HOO CEO Rexy Wang on Twitter on July 15, Hoo employee and former Binance head of security Fang Wenbin (known as "Top") "took advantage of his position at Hoo to delete the company system privately, causing everyone in the company to be unable to access the system, resulting in a temporary failure of the main domain name". Top replied to allege that, "Rexy himself has transferred most of the assets from the platform. Employee salaries and platform users cannot withdraw coins".

At some point after that, Wang made his Twitter private. Hoo's social media channels have been inactive. On November 18, the exchange website was replaced with a post that identified the "Hoo de facto controller", Xu Tong Hua, and said: "Currently all permissions for Hoo's wallet and website programs are controlled by Mr Xu, so please contact the official email if you have any questions."

Meanwhile, customers have been active on social media complaining about the apparent fraud, and some have formed an informal group pushing for legal action against Hoo.

Coinhouse suspends "savings accounts" due to Genesis suspension due to FTX collapse

The French crypto broker Coinhouse announced that they would be suspending withdrawals from their crypto "savings account" product. Coinhouse partners with Genesis to offer the service, and Genesis recently suspended their service due to the FTX collapse. As a result, services that relied on Genesis, including Gemini and now Coinhouse, are halting their own services as the dominoes continue to fall.

Australian Securities Exchange scraps its $167 million, seven-year-long blockchain project

The Australian Securities Exchange (ASX) has finally pulled the plug on their project that would have replaced the aging CHESS system that is used for transfer and settlement. The group had spent seven years and AU$250 million (US$167 million) on a private blockchain project, which has suffered repeated delays and setbacks. A recent, third-party report by Accenture on the project estimated that it was only 63% complete, and was excessively complex, "including in the way ASX requirements interact with the application and underlying ledger". The project has grappled with issues including lack of throughput to settle trades.

ASX will write off the AU$245–$255 million (US$164–$170M) they have poured into the project, and start again on designing a replacement for the CHESS system.

- "ASX kills its blockchain project, will write off $250 million", Financial Review

Class action lawsuit filed against celebrities who promoted FTX

A class action lawsuit has been filed against Sam Bankman-Fried and a slew of celebrities who helped to promote FTX as a safe place to hold and trade crypto. Defendants include Tom Brady, Gisele Bündchen, Steph

Curry, Shaquille O'Neal, David Ortiz, Naomi Osaka, and Larry David.

The suit alleges that the celebrities violated the anti-touting provisions of securities laws by failing to disclose the nature, scope, and amount they were compensated to promote the platform.

Nigerian startup Nestcoin has nearly all funds locked in FTX, announces layoffs

Nestcoin, a Nigerian startup that both builds and invests products they hope will "democratis[e] access to economic opportunity for everyday people in frontier markets", has announced that they will lay off more than 50% of their nearly 100 employees. Remaining employees will see their pay slashed by 40%, and the company CEO plans to take no compensation at all.

Nestcoin had nearly all of the funds remaining from their $6.45 million funding round locked in FTX — approximately $4 million.

Gemini halts withdrawals from their lending service

The Gemini cryptocurrency platform announced that they would be pausing withdrawals on their lending platform. This is because they partner closely with Genesis' lending products, which halted withdrawals shortly before.

The company said in a blog post that they were "working with the Genesis team" to restore withdrawals. Like Genesis, they tried to urge that the issue would not affect other Gemini products. However, a service outage that same day did little to strengthen trust in the company.

Genesis crypto lending service halts withdrawals

The crypto lending portion of Genesis Global Trading announced they would be halting withdrawals in the wake of the "extreme market dislocation and loss of industry confidence caused by the FTX implosion". On Twitter, they wrote that "FTX has created unprecedented market turmoil, resulting in abnormal withdrawal requests which have exceeded our current liquidity."

They urged in their announcement that the decision would not impact their trading or custody businesses — though if I was a user of their other services I might not be feeling so reassured given crypto companies' poor track record of segregating operations.

Genesis has about $2.8 billion in total active loans as of the end of September 2022.

This is not the first crisis for Genesis this year. The firm lost hundreds of millions due to exposure to the Three Arrows Capital collapse, and in August announced layoffs of 20% of their employees.

Coachella NFTs stop working due to FTX collapse

Coachella partnered with FTX to sell a collection of NFTs in February, ultimately raking in around $1.5 million. The NFTs were paired with physical items — Coachella passes, art prints, and photo books — and the NFT owners had the option to "redeem" their NFT to receive the item. However, all of this was done through FTX, and with FTX no longer fully operational, redemptions are no longer possible. The FTX server storing the artwork for the NFTs was also intermittently available, so holders reported seeing broken images when going to view their NFT.

Ten of the NFTs in the collection came with lifetime passes to Coachella, and sold for six figures. Each year, the NFT holder has to go through the redemption process to obtain their festival pass.

Many of the token owners bought their NFTs with FTX and simply left them in their accounts on the platform. Some were able to transfer their tokens before FTX's NFT platform stopped operating, but many did not.

Australian crypto exchange Digital Surge suspends withdrawals

The Brisbane-based cryptocurrency exchange Digital Surge announced that they would be suspending deposits and withdrawals. "Due to the impact of FTX Australia's administration, we are not able to operate business as usual and have suspended all deposits and withdrawals until further notice," they wrote. They also disclosed in an email that they had "some limited exposure to FTX".

- "Aust crypto exchange suspends withdrawals", Shepparton News

BlockFi plans layoffs, possible bankruptcy after FTX collapse

Cryptocurrency lending company BlockFi suspended withdrawals on November 10 after the FTX collapse, an expected move since they had stayed afloat after the previous crypto meltdown only thanks to hundreds of millions in loans from FTX.

Now, the Wall Street Journal reports that BlockFi has been considering layoffs, and has been in talks with bankruptcy attorneys about a possible Chapter 11 filing.

Although BlockFi disputed reports that they had been custodying client assets at FTX, they acknowledged that they had "significant exposure to FTX and associated corporate entities that encompasses obligations owed to us by Alameda, assets held at FTX.com, and undrawn amounts from our credit line with FTX.US".

- "BlockFi Prepares for Potential Bankruptcy as Crypto Contagion Spreads", The Wall Street Journal

SALT crypto lender halts their service

The crypto lending firm SALT announced that they would be halting withdrawals due to exposure to FTX. "I am sorry to report that the collapse of FTX has impacted our business," they wrote in a message to users. "Until we are able to determine the extent of this impact with specific details that we feel confident are factually accurate, we have paused deposits and withdrawals on the SALT platform effective immediately."

Binance announces an "industry recovery fund"

CZ of Binance announced on Twitter that Binance would be forming an "industry recovery fund", which he says is intended for projects that are "otherwise strong, but in a liquidity crisis".

This not entirely unlike someone trying to sell you a house that is "otherwise sturdy, but in an engulfed-in-flames crisis".

He says the project is intended to reduce the "cascading negative effects of FTX", underscoring how nervous this whole debacle is making other players in the industry.

Ikigai Asset Management announces "large majority" of assets trapped in FTX

The founder and chief investment officer of the Californian crypto hedge fund Ikigai Asset Management wrote on Twitter, "Last week Ikigai was caught up in the FTX collapse. We had a large majority of the hedge fund's total assets on FTX. By the time we went to withdraw Monday mrng, we got very little out. We're now stuck alongside everyone else."

He announced that they would continue trading their remaining assets, and continue operating their venture fund. However, he said the future of the hedge fund was unclear, and likely to depend on what happens with FTX customer withdrawals.

"I'm pretty disgusted with the space as a whole and kinda humanity in general," he continued. "I'm at a loss for words at the depth & breadth of the pieces of shit that permeate crypto. So many fucking sociopaths were granted the opportunity to do so much damage. It's hard for me to imagine the space bouncing back quickly from this ordeal. Too many got burned too hard."

Huobi exchange announces $18.1 million is locked on FTX, mostly customer funds

Huobi announced to shareholders that they had $18.1 million in crypto assets on the FTX exchange, where they can't be withdrawn. They reported that approximately $13.2 million of those funds were customer assets. They announced that they would be taking an unsecured loan of up to $14 million from controlling shareholder Li Lin to cover the client assets.

AAX cryptocurrency exchange suspends withdrawals

The Hong Kong-headquartered cryptocurrency exchange announced that they would suspend withdrawals, which they claimed was due to a system upgrade that went poorly. They've estimated it will taken seven to ten days for normal service to resume.

Users have been hesitant to believe this explanation, given the enormous shakeup in the industry lately, and the tendency for firms to be less-than-forthcoming when they are in major crisis.

Three days prior, the company had published a blog post claiming that AAX had no exposure to FTX and its affiliated companies, that AAX had stable reserves, and that user funds were never exposed to counterparty risk.

Flare token rug pulls or is exploited for $17 million

Exploits and rug pulls of random tokens on BNB Chain are fairly commonplace, but typically the amount of money lost is fairly minimal. In this case, exploiters or insiders were able to siphon 3.9 billion $FLARE from the Flare project, which they swapped for just under $17 million.

This serves as a good example of how theft amounts shouldn't be naively calculated based on the token price before the theft × the number of tokens stolen. $FLARE was priced at around $18.25 before the attack, and a naive calculation would place the theft amount at $71 billion. However, the lack of liquidity caused the token price to plummet to $0.0000018, and the attacker ultimately ended up with around $17 million.

Over $4 million drained from DeFiAI

"Our contract has been hacked and has caused a lot of losses," wrote DeFiAI simply in their announcement. That same day, the project had announced the launch of a new website for their project.

The total funds stolen appear to be around $4.17 million, according to analysis by SlowMist.

- Tweet by DeFiAI

- Analysis by Slowmist

Tokensoft intentionally publishes personal data of around 5,000 users who they believe are "bad actors"

Tokensoft is a project that aims to help web3 projects launch fairly, without the launches being gamed. The group evidently thought they had come across 5,000 or so users who had been gaming airdrops, to which their solution was to publish a list of private user data about those individuals. The list included full names, wallet addresses, and physical and IP addresses.

Several users replied to the message in shock that their data was exposed, saying they'd never done anything wrong. The Tokensoft employee replied, "If you made it on the naughty list...yes, shame on you....I shared your info, better luck next time".

The project later deleted the link from the Discord server, then tried to claim that it had never been posted at all, then issued a statement that "information was mistakenly posted in Tokensoft's social media channels".

Bahamas Securities Commission issues statement that they didn't instruct FTX to process withdrawals for Bahamian customers

The Securities Commission of the Bahamas issued a statement saying that "The Commission wishes to advise that it has not directed, authorized or suggested to [FTX] the prioritization of withdrawals for Bahamian clients."

This contradicted FTX's previous statement that "Per our Bahamian HQ's regulation and regulators, we have begun to facilitate withdrawals of Bahamian funds." The announcement that they would be processing withdrawals for Bahamian customers led to a slew of non-Bahamian customers trying to find ways to withdraw their funds via bribes and shady NFT deals.

Some have viewed FTX's choice to enable Bahamian withdrawals as evidence that they were trying to allow FTX employees and family members to get access to their funds on the exchange, even when most customers had no such access.

Crypto.com CEO admits company accidentally sent 320,000 ETH ($416 million) to another crypto exchange a few weeks prior

A Twitter user posted Etherscan screenshots showing a massive flow of crypto from the Crypto.com cryptocurrency exchange to another exchange, Gate.io. "Anyone know why Crypto.com would send 320k ETH (82% of their ETH today) to Gate.io on October 21?", they wrote. "And why Gate.io would send back to Crypto.com 285K ETH 5-7 days later?"

Crypto.com's CEO, Kris Marszalek, replied: "It was supposed to be a move to a new cold storage address, but was sent to a whitelisted external exchange address. We worked with Gate team and the funds were subsequently returned to our cold storage." He later clarified that all of the funds were returned.

Twitter users, reasonably, reacted in horror at the revelation that the platform had accidentally sent such a substantial portion of their funds elsewhere in a careless mistake, and that such a monumental mistake was even possible. They were lucky that they erroneously sent the funds to another exchange, and one who agreed to return the funds.

This is not the first time Crypto.com has erroneously transferred funds; in August of this year, they sued a woman to whom they'd accidentally sent $7.2 million that wasn't hers.

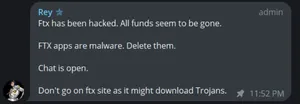

FTX claims it was hacked as more than $400 million is withdrawn

Over $477 million was mysteriously withdrawn from FTX and FTX US late on November 11, despite the company freezing withdrawals.

An FTX account administrator wrote on the FTX support Telegram, "FTX has been hacked. FTX apps are malware. Delete them. Chat is open. Don't go on FTX site as it might download Trojans". The message was pinned by FTX General Counsel Ryne Miller.

Miller later wrote on Twitter, "Investigating abnormalities with wallet movements related to consolidation of ftx balances across exchanges - unclear facts as other movements not clear. Will share more info as soon as we have it."

A Telegram admin subsequently wrote, "Not all hope is lost. Engineers have managed to retrieve substantial amount of funds," but no details were provided beyond that. A later announcement by Miller claimed that FTX had "initiated precautionary steps to move all digital assets to cold storage", suggesting some of the transfers may have been a part of that effort.

Many speculated that the so-called hack had been coordinated by insiders.

FTX files for bankruptcy, Sam Bankman-Fried resigns

Aaaand there it goes.

FTX announced that it had filed for Chapter 11 bankruptcy in the United States. Sam Bankman-Fried resigned as CEO.

SBF had spoken about trying to raise additional funds. In leaked Slack messages, he had allegedly written that "One could maybe say, if they wanted to be optimistic, that we have a lot theoretically in and/or potentially for the raise". No one was actually saying this.

Early crypto investor loses $42 million in wallet compromise

Bo Shen, a general partner at Fenbushi Capital and an early adopter of cryptocurrencies, tweeted on November 22 that two weeks prior, someone had stolen $42 million in cryptocurrencies from his personal wallet. "The stolen assets are personal funds and do not affect on Fenbushi related entities," he wrote.

Analysis by the crypto security firm SlowMist attributed the theft to a compromise of Shen's seed phrase. Shen had been using the Trust Wallet software, though the theft does not appear to be related to security issues with the wallet software.

Users attempt to circumvent FTX withdrawal freeze with bribes and NFTs

Users panicked when FTX stopped processing withdrawals, particularly those with substantial amounts of funds locked in the exchange. When the exchange tweeted that they had "begun to facilitate withdrawals of Bahamian funds", some saw an opportunity.

"Any FTX employees willing to change my accounts country of residence to Bahamas to facilitate withdrawal I am offering $1 million and unlimited legal fees", wrote one trader (who later claimed to be joking).

A popular crypto Twitter user named "Algod" offered $100,000 to any FTX employee who would process their KYC documents, allowing them to withdraw. He was subsequently seen to be successfully withdrawing over $2 million in assets from the platform. He also shared links to a Telegram group where his partner was offering to buy people's FTX accounts for 10¢ on the dollar, from customers who feared they may never see the money again, or would only regain access to a fraction of it after years of court proceedings. Algod later denied "erroneous and defamatory statements" that he'd bought discounted claims/assets", admitting that he'd considered it, but claiming he ultimately decided not to.

Some observers noticed over $21 million withdrawn via NFT trades, that appeared to be being used as a way to bypass the internal blocks on users transferring balances to one another. People with funds locked in FTX bought NFTs from Bahamas-based users, spending their full account balance on the NFT and thus enabling the Bahamian user to then withdraw the funds. "This appears to be the first recorded case of NFT utility in existence 👍", wrote Cobie.

The Securities Commission of the Bahamas freezes FTX assets, appoints provisional liquidator

The Securities Commission of the Bahamas (where FTX is headquartered) announced they had frozen the assets of FTX and "related parties" — presumably Alameda. They also disclosed that they had suspended FTX's registration, and appointed a provisional liquidator.

The announcement went on to say, "The Commission is aware of public statements suggesting that clients' assets were mishandled, mismanaged and/or transferred to Alameda Research. Based on the Commission's information, any such actions would have been contrary to normal governance, without client consent and potentially unlawful."

- Media release by the Securities Commission of the Bahamas

DFX Finance suffers $5 million loss

An attacker was able to use a flash loan to exploit a vulnerability in the smart contract for DFX Finance, a decentralized forex trading platform. The platform suffered a loss amounting to around $5 million. The attacker subsequently laundered the funds through the Tornado Cash cryptocurrency tumbler. The attacker didn't make off with the entire amount lost from the platform, partly due to an MEV bot snagging a significant amount of the funds.

BlockFi suspends withdrawals

BlockFi had a tough time this past June, floundering after substantial losses in the crypto downturn. They were bailed out by FTX, who extended them a $250 million loan, then shortly after reached a deal that would give them the option to acquire BlockFi, and also extended BlockFi $400 million in revolving credit.

Now, the bailer is the one requiring the bailing, and the possible bailout of FTX by Binance fell through. This means that BlockFi is in a tough and uncertain spot, which is why they announced through Twitter that "until there is further clarity, we are limiting platform activity, including pausing client withdrawals". They also wrote that they had learned about the FTX collapse via Twitter.

BlockFi founder and COO Flori Marquez had tweeted only two days prior, just after the FTX news, that "All BlockFi products are fully operational. BlockFi is an independent business entity. We have a $400MM line of credit from FTX.US (not FTX.com) and will remain an independent entity until at least July 2023. We are processing all client withdrawals."

The Binance/FTX deal is off

It's over as quickly as it started, and it started pretty dang quickly. Binance walked away from the non-binding letter of intent that Binance signed to acquire FTX, which doesn't come as a huge surprise given how much they couched the announcement in caveats that it was subject to due diligence and that Binance could exit any time.

According to Binance, "As a result of corporate due diligence, as well as the latest news reports regarding mishandled customer funds and alleged US agency investigations, we have decided that we will not pursue the potential acquisition of FTX.com."

FTX is really up a creek. Reports suggest that the hole on their balance sheet is looking like $8 billion, a circumstance that is certainly not improving as FTT prices continue to plummet.

There is still no news about what will happen to Alameda, but the SBF-owned quant firm's website has ominously been taken offline.

- Tweet by Binance

- "Binance Walks Away From Deal to Rescue FTX", The Wall Street Journal

FTX is insolvent; Binance offers bailout

Surprising just about everyone, FTX's Sam Bankman-Fried and Binance's Changpeng "CZ" Zhao announced suddenly that Binance had signed a "non-binding [letter of intent], intending to fully acquire FTX.com" after a "liquidity crunch". FTX, a major crypto exchange, had recently been rumored to be insolvent, and had stopped processing withdrawals earlier that day.

It appears that the Binance move was a last-ditch effort to save FTX, which went from being a powerful player in the crypto market offering bailouts and looking to acquire bankrupt companies to an insolvent exchange struggling to stay afloat in an incredibly short period of time.

CZ of Binance hedged a bit in his announcement, underscoring that "Binance has the discretion to pull out from the deal at any time" and would be performing "full [due diligence]" before the deal moved forward. It's not yet clear how much the Binance sell-off of FTX tokens contributed to the instability of the exchange.

Speculation emerges around Alameda Research and FTX solvency; Binance liquidates holdings

On November 2, CoinDesk published a leaked balance sheet from Alameda Research (a trading firm also owned by FTX founder and CEO Sam Bankman-Fried). The sheet suggested that Alameda held substantial amounts of FTX's $FTT token. "While there is nothing per se untoward or wrong about that, it shows Bankman-Fried's trading giant Alameda rests on a foundation largely made up of a coin that a sister company invented, not an independent asset like a fiat currency or another crypto," CoinDesk wrote.

Following the report, Binance CEO Changpeng "CZ" Zhao announced they would be liquidating their FTT holdings. CZ also took a shot at SBF's recent controversial policy recommendations, writing, "Liquidating our FTT is just post-exit risk management, learning from LUNA. We gave support before, but we won't pretend to make love after divorce. We are not against anyone. But we won't support people who lobby against other industry players behind their backs."

SBF first appeared conciliatory towards Binance, writing "I respect the hell out of what y'all have done to build the industry as we see it today, whether or not they reciprocate, and whether or not we use the same methods. Including CZ. Anyway -- as always -- it's time to build. Make love (and blockchain), not war." However, he later wrote that "A competitor is trying to go after us with false rumors" and urged that "FTX is fine. Assets are fine."

Federal judge rules that LBRY sold tokens in violation of federal securities laws

LBRY is a blockchain-based social network and video sharing protocol that was described by a researcher at The International Centre for the Study of Radicalisation and Political Violence as "the new YouTube for the far-right" in 2021.

In March 2021, the SEC sued LBRY over their LBC tokens, which were used for paid streaming, tipping, and as rewards for using the platform inviting other users. On November 7, 2022, a federal judge of the District Court for the District of New Hampshire ruled that "because no reasonable trier of fact could reject the SEC's contention that LBRY offered LBC as a security, and LBRY does not have a triable defense that it lacked fair notice, the SEC is entitled to judgment." The judge granted the SEC's motion for summary judgment, meaning the case will not go to trial.

U.S. Attorney convicts individual in 2012 theft from the Silk Road, announces seizure of over 50,000 Bitcoin priced at more than $1 billion

The U.S. Attorney's Office for the Southern District of New York announced that they had convicted James Zhong with wire fraud pertaining to his 2012 theft of around 50,000 Bitcoin from the Silk Road online marketplace. Zhong pled guilty to one count of wire fraud.

The government has filed a motion in the case against Ross Ulbricht, the founder and operator of the Silk Road who is serving life in prison, seeking to retain the seized Bitcoin. At the time of seizure in November 2021, the Bitcoin were notionally worth $3.36 billion. On the date the charges were announced, they would be notionally worth $1.06 billion.

- "U.S. Attorney Announces Historic $3.36 Billion Cryptocurrency Seizure And Conviction In Connection With Silk Road Dark Web Fraud", U.S. Attorney's Office for the Southern District of New York

Pando exploited for $20 million

The defi protocol Pando suffered a $20 million loss when it was exploited with an oracle manipulation attack. The protocol suspended several of its projects in response to the hack, and wrote that they hoped to negotiate with the hacker to regain some of the stolen proceeds. Some of the stolen funds were able to be locked, although it's not clear if it was the total amount.

Telegram repossesses usernames so they can sell them as NFTs

In August, the popular messaging app Telegram started repossessing some desirable usernames that were already being used. Shortly afterwards, Telegram founder Pavel Durov explained that he had been impressed by a quarter-million-dollar domain sale by the TON blockchain domain project, and wrote, "Let's see if we can add a little bit of Web 3.0 to Telegram in the coming weeks."

Telegram later introduced some of the repossessed usernames for sale as pricey NFTs on their new "collectible usernames" market, dubbed Fragment. Although Durov had claimed that "70% of all Telegram usernames had been reserved in inactive channels by cybersquatters from Iran", and that the only usernames that were "withdrawn" had been out of use, users were given no warning or option to keep their names.

On October 27, Durov announced that "in a few days, we will also introduce the ability for users to sell their existing usernames on Fragment" — unwelcome news for those whose usernames were sold out from under them by Telegram.

Some of the usernames that have sold on the marketplace include brand names like Facebook (which sold for 60,000 TON, or ~$94,200), FIFA (sold for 600,000 TON, or ~$972,000), Amazon (sold for 262,500 TON, or ~$425,000), and Meta (sold for 404,000 TON, or ~$723,000). There is no indication the buyers are necessarily associated with the brands in question. Furthermore, the username marketplace is not available in the USA.

Monkey Drainer steals dozens more NFTs, nets around $867,000

The "Monkey Drainer" NFT phishing scammer first identified by blockchain detective zachxbt has struck again. They successfully emptied 7 CryptoPunks and 20 Otherside NFTs, which they flipped for 522 ETH (~$867,000). The scammer then laundered the funds through the Tornado Cash cryptocurrency mixer.