bDollar stablecoin suffers $730,000 price manipulation attack

bDollar was the first algorithmic stablecoin on the BSC blockchain. An attacker was able to manipulate the price of underlying assets to pull 2,381 wBNB out of the protocol, worth around $730,000. The project had been audited by CertiK.

- "又一算稳项目被攻击,bDollar损失约73万美元", DefiDaoNews

Class action lawsuit filed against HUMBL blockchain platform

A litigation firm filed a class action lawsuit against HUMBL, a financial services company that touts its web3 and defi products. The lawsuit alleges that HUMBL and its executives made false and misleading statements about the company and its prospects, made "selectively timed announcements to keep Humbl stock price high so that Company insiders could sell off their holdings into artificially created volume", and sold its BLOCK ETX assets in violation of securities laws.

HUMBL stock has dropped from a high of $6.84 per share to a low of $0.11. Similarly the BLOCK ETX asset has dropped more than 87% from its high.

- HUMBL lawsuit website

Doodled Dragons serial rug-puller revealed to be behind yet another Solana project

The serial rug-puller who was behind the Balloonsville rug pull in February and Doodled Dragons rug pull in January has popped up once again, this time with a Solana NFT project called Reptilian Renegades. A project called Hydra Launchpad, which had recently announced they would be adding Reptilian Renegades to their lineup, were the ones to expose the project team member, who went by "Fuopist" on this project. Hydra claimed that they had been able to take control of the project's mint authority and cut off Fuopist from receiving further proceeds from the project.

After the Balloonsville rug pull, which used the Magic Eden NFT marketplace, Magic Eden announced they would no longer be accepting anonymous projects on their platform. Despite that, this person was able to launch Reptilian Renegades on Magic Eden, where they were able to get their account verified.

Following the unmasking, the Reptilian Renegades Twitter account posted a slew of tweets supposedly exposing various NFT influencers for shady behavior including undisclosed promotions. "I'm literally the Batman. I stop crime whilst committing crimes," they wrote in response to a person who tweeted, "The balloonsville guy is back and he's ready to tell you how corrupt NFTs are while he steals from you. The lack of self awareness is truly next level."

Users threaten to sue after yield generation project Stablegains loses $44 million in Terra collapse

A class action law firm sent a letter to the yield generation project Stablegains, demanding records on customer accounts, marketing and advertising strategies, and communications relating to the Terra stablecoin. Stablegains described itself as aiming to "make it simple and safe for everyone to benefit from advances in financial technology", and promised that "regardless if crypto markets are soaring or crashing, the value of assets under our management remains stable".

Unfortunately for their customers, it turned out that Stablegains was heavily invested in the Terra project's Anchor protocol, which collapsed along with the rest of the Terra ecosystem last week. Stablegains' website had stated they primarily generated yields through the asset-backed stablecoin USDC. However, after the collapse of Terra, Stablegains admitted that "All users' holdings are in UST" — which lost over 90% of its value.

"Quantum-resistant" blockchain QAN suffers bridge attack

The $QANX token for the QAN project suddenly plummeted in value as an attacker stole more than 4 million QANX from the project. The attacker subsequently swapped the tokens for around 370 ETH ($707,000). In a video posted to Twitter, the project CEO stated that it was "definitely a bridge issue", and that they'd shut down the project's bridge. They also said they had contacted exchanges to freeze the wallets that had been involved in the "issue".

QAN describes itself as a blockchain that helps "resist quantum attacks", though apparently not the types of bridge attacks that have become fairly common in the past year or so.

Class action lawsuits filed against Terra founders after crypto collapse

Following the collapse of the Terra ecosystem and its tokens TerraUSD and Luna, affected Korean investors have filed both criminal and civil lawsuits against the project's creator, Do Kwon. Represented by RKB & Partners, the lawsuit seeks to seize Kwon's assets and pursue fraud charges.

Another Korean group, calling themselves "Victims of Luna, UST coins", has amassed 1,500 members and reportedly plans to file a lawsuit against Kwon and Terraform Labs' other cofounder, Shin Hyun-Seong (who is also known as Daniel Shin, and is no longer with Terraform Labs).

This development may be particularly inconvenient for Kwon and Shin, given Terra's legal team quit the company the previous day.

On June 17, another investor filed a separate lawsuit against Terraform Labs, Kwon, and various others in a US court.

"Feminist Metaverse" token exploited for $533,000

The "Feminist Metaverse" ($FM) token suddenly plunged in value by 99.7% after an attacker stole 1,838 BNB ($533,000). The hacker quickly transferred the stolen funds to the Tornado Cash tumbler to help hide their tracks.

The project advertised on its website its plans to "Create Feminist economics in the form of a DAO to balance the male-dominated world." The project's whitepaper explains how the metaverse will apparently "greatly reduce the impacts on women's normal work and inequality in wages brought by their physiological differences and pregnancy. As a consequence, it helps eliminating a number of unresolved problems in the real world like gender discrimination, inequality in wages, sexual harassments, sexual assaults, trafficking of women and child marriage." It's not clear what specifically the "Feminist Metaverse" project was hoping to achieve.

Fake minting links distributed after several large NFT Discord servers are compromised

Members of several large NFT Discord servers began seeing suspicious-looking messages announcing supposed NFT mints that turned out to be fakes. Affected communities appeared to include Moonbirds/PROOF, Axie Infinity, RTFKT, Memeland, Alien Frens, and others. The attack appeared to involve a Discord bot called MEE6, though there was some confusion around whether there was a compromise of MEE6 itself or if it was simply used in the attack. The following day, MEE6 acknowledged that an employee account had been compromised.

Bot compromises have emerged as a wide attack vector in crypto and web3 communities, as widely-used bots can have elevated permissions across Discord channels used as official information sources across many communities.

Terraform Labs' legal team resigns

In what seems like a bad sign for Terraform Labs, the developer of the Terra blockchain and the TerraUSD (UST) and Luna cryptocurrencies, the three members of the company's legal team left the company. This came shortly after UST, Luna, and the entire Terra ecosystem dramatically collapsed after the stablecoin lost its peg last week.

Four pricey NFTs stolen from actor Seth Green, complicating his plans for an animated series

Actor Seth Green tweeted that he had been targeted with a phishing attack that resulted in the theft of four pricey NFTs: a Bored Ape, two Mutant Apes, and a Doodle. The thief quickly flipped three of the four NFTs for sale, netting 145.5 ETH (about $300,000).

The theft occurred on May 8, though Green only seemed to notice on May 17 when he tweeted, "Well frens it happened to me. Got phished and had 4NFT stolen."

The loss of the Bored Ape was later revealed to have put Green in a bit of a pickle, when he released the trailer for a new animated series he was developing that starred his pilfered primate. Given that BAYC ownership grants commercial usage rights (which are presumably transferred to the new owners when the NFT changes hands), the person who bought the NFT flipped by the phisher could have possibly brought a lawsuit against Green if he moved forward with the series.

Green ultimately spent about $300,000 to buy his ape back from the hacker.

American running "untraceable" service "designed to evade US sanctions" is charged after being traced

An unidentified US citizen transferred more than $10 million in Bitcoin to a cryptocurrency exchange in a "comprehensively sanctioned" country where they were running a payments platform. They advertised that transactions through the platform were untraceable, and described the platform as designed to evade U.S. sanctions. Despite this, law enforcement was able to obtain information from U.S. and foreign cryptocurrency exchanges — including KYC information provided by the individual — to help identify and trace the individual behind it.

Though the country is as yet unnamed, the limited number of countries sanctioned in the way described in the decision allow us to deduce that it was either Cuba, Iran, North Korea, Syria, or Russia. This case marked the D.O.J.'s first criminal prosecution involving alleged use of crypto to evade sanctions.

U.S. Magistrate Judge Zia M. Faruqui wrote in the opinion: "Virtual currency is traceable. Yet like Jason Voorhees the myth of virtual currency's anonymity refuses to die. See Friday the 13th (Paramount Pictures 1980)."

Scream lending protocol racks up $35 million in bad debt after hardcoding not-so-stablecoin prices to $1

The defi lending protocol Scream may have taken the "stable" in "stablecoin" a bit too literally when they hardcoded the prices of the Fantom USD (fUSD) and DEI stablecoins. In the past few weeks we've seen many stablecoins wobble, and when fUSD and DEI followed suit, Scream ended up in trouble. Users were able to take advantage of the inaccurately high price to borrow other stablecoins on the cheap, leaving Scream with $35 million in bad debt. The platform's reserves of other stablecoins were completely drained; meanwhile, Scream users holding fUSD or DEI can't withdraw.

CZ admits Binance held Luna and UST in bizarre tweet threads

On May 15, Binance CEO Changpeng Zhao (widely known as CZ) created a tweet thread in which he attempted to speak nonchalantly about questions that had "just occurred to [him]" about whether Binance held any UST. In the thread he attempted to distance himself from decisions or knowledge around such holdings, speaking cavalierly about how "we probably do have some". Former FBI agent James Harris wrote an interesting analysis of the thread, concluding, "If people weren't worried before, they will be now. If investigators weren't suspicious before, they should be now."

The following day, CZ tweeted, "Binance received 15,000,000 LUNA (at peak worth $1.6 billion USD, now not much) as part of the original ($3m) invest. 560x return at peak." In this tweet, "not much" glossed over the fact that these LUNA, obtained in return for a $3 million investment and at one point nominally worth $1.6 billion, are now worth $2,900.

He also wrote that Binance had 12,000,000 UST — worth $12 million when UST was properly pegged, and now worth $1.16 million (assuming liquidity exists to sell it at all).

Luna Foundation Guard reports what it did with its Bitcoin reserves, raising more questions

Many were eagerly awaiting a report from Luna Foundation Guard (LFG) on what happened to the several billion dollars' worth of Bitcoin reserves they once held, which they transferred during the UST collapse. The organization tweeted an explanation of the actions they took with those funds on May 16, describing how they began to convert Bitcoin to UST. They referred to transferring BTC and other reserves to "a counterparty", who traded them UST in exchange. They didn't name who these counterparties were.

More than a few people were unsatisfied with this reporting, asking more transparency around who these "counterparties" were. Ultimately, this action benefited the "counterparties", providing liquidity to these whales who were able to exit their now risky UST positions for a good price, and did not help most of the individuals holding UST.

"Stable"coin DEI loses peg

Another stablecoin lost its peg as dominoes continued to fall in the declining crypto market. DEI, an algorithmic stablecoin created by Deus Finance on the Fantom network, de-pegged on May 15. Intended to be pegged to the US dollar, the token dipped to a low of around $0.50, and continued to hover well below its intended price through the next day. DEI had a nominal market cap of more than $88 million before losing its peg.

This is another bump in the road for Deus Finance, which lost a total of $16.4 million in two separate flash loan attacks in March and April 2022.

Flash loan attacks on "Feed Every Gorilla" token take $1.9 million

A flash loan attack on the "Feed Every Gorilla" (FEG) token swap contracts pulled $1.3 million from the project, also tanking the token price by 80%. The project operates on both the Ethereum and BSC chains, and the attacker was able to use the exploit against the contracts on both networks. Shortly after the first attack, FEG was hit with a second flash loan attack that drained another $590,000 from the project.

Prior to these attacks, FEG had earned some notoriety from a May 2021 Vanity Fair article outlining an alleged pump-and-dump scheme, titled "Inside the Rise and Fall (and Rise and Fall) of Shit Coins". Despite the bad press, much of the FEG community maintained that the article was a smear and nothing more than an attempt by the author to create FUD. "You could literally take every token and this would apply to everyone..." wrote a moderator of the official FEG subreddit.

People continue to wait for a public accounting of what happened to Terra's $3.5 billion in Bitcoin reserves

Now that the dust is settling somewhat from the dramatic collapse of Terra, people are beginning to wonder when they'll hear more about what exactly happened to the 80,394 Bitcoin (priced at $3.5 billion at time of purchase; priced closer to $2.5 billion at the time of writing this entry) that previously belonged to Luna Foundation Guard (LFG). The project had previously purchased the assets to hold as reserves, and as UST began to lose its peg, LFG announced they would use those reserves to buy UST to help maintain the peg. Over the next few days, the reserves were emptied, but after they were moved to the Gemini exchange they became impossible to trace further. Although transactions are usually quite traceable on the blockchain, when funds are moved to services like the Gemini exchange, they become impossible to trace using public data because of how exchanges pool funds and transactions internally.

Terraform Labs CEO Do Kwon tweeted on May 13 that "We are currently working on documenting the use of the LFG BTC reserves during the depegging event. Please be patient with us as our teams are juggling multiple tasks at the same time." It's not clear when this documentation will be released. Binance CEO Changpeng Zhao joined the group of people asking about the BTC reserves, tweeting, "I would like to see more transparency from them. Much more! Including specific on-chain transactions (txids) of all the funds. Relying on 3rd party analysis is not sufficient or accurate."

Blockchain insurance company InsurAce shortens their claims window for Terra holders to just a week

InsurAce is a defi insurance provider (oh yes, they exist) that allows people to buy insurance against events including smart contract vulnerabilities and stablecoin depegs. Following the Terra collapse, InsurAce suddenly announced that its customers who held Terra had only a week to file claims, and that "Late submission [sic] will be rejected without further appeal".

Altogether, InsurAce says they paid out about $11 million to around 173 claimants as a result of the depeg. Evidently there were 61 others who did not submit their claims within the deadline.

SpiritSwap is the latest victim of a domain hijacking attack

In what is beginning to become a pattern, SpiritSwap was the latest project where attackers gained control of their domain and were able to modify the frontend to divert funds to a wallet under their own control. SpiritSwap tweeted that the "the hacker has managed to exploit Godaddy" (unlikely — it was more likely a case of stolen credentials) and swap out the recipient address.

The hacker only managed to exfiltrate around $18,000 before being discovered, and SpiritSwap shut down their swapping through their router to prevent the attack from continuing.

MM.Finance suffered a similar attack earlier in the month, losing $2 million after an attacker gained control of the domain and swapped in their own address to siphon funds.

Phishing attack targets users of sites including Etherscan and CoinGecko

Popular cryptocurrency websites including Etherscan, CoinGecko, and DeFi Pulse were showing users a pop-up prompting them to connect their MetaMask wallets. CoinGecko founder Bobby Ong stated that he believed the culprit was a malicious advertising script from a crypto ad network called Coinzilla. The advertisement appeared to be from a site mimicking the popular Bored Apes Yacht Club NFT project, which was taken down after the scam was discovered. It's as yet unclear how many users accepted the prompt, or what malicious actions (if any) were taken.

Crypto.com reverses some Luna trades, offers $10 consolation prize

One of the features of crypto that its proponents sometimes highlight is that transactions can't be reversed. This, of course, is not true when making trades on exchanges like Crypto.com, who can largely do whatever they want with the wallets they maintain and the coins they keep track of on users' behalf.

On May 13, the company announced it would be reversing transactions made during an hour-long period on May 12 when "users who traded LUNA were quoted an incorrect price". Some users were able to profit off the discrepancy, but later were told that their transactions were being reversed. Crypto.com offered $10 in CRO, their cryptocurrency token, "for the inconvenience caused". Crypto.com halted Luna trading after discovering the issue, and it remains halted as of May 13.

The issue sounds quite similar to issues that affected various defi projects around the same time. Several projects who failed to account for unexpected Luna price data coming from blockchain oracles including Chainlink suffered major attacks.

- "LUNA Trading Incident on Crypto.com App", Crypto.com

Unexpected oracle data in the wake of Terra blockchain halt enables multiple attacks on other platforms

Earlier today, Terra halted their blockchain after a devastating few days. Subsequently, Chainlink's oracle paused the price feed, causing it to fall out of sync with the apparent market price of the token. This enabled multiple attacks on various platforms.

$13.5 million was fraudulently borrowed from the Venus protocol on BSC. Blizz Finance on Avalanche reported their protocol had been entirely drained, amounting to around $8.3 million. Blizz subsequently announced in a post-mortem that "Blizz has no treasury or development fund and a significant portion of the stolen assets belonged to our team. As such we regret to announce the protocol has been paused and we do not intend to resume operations."

FBI charges EminiFX CEO with fraud

Eddy Alexandre, CEO of the cryptocurrency and forex trading platform EminiFX, was charged by the FBI with fraud for his role in what he described to investors as a crypto investment scheme. Promising to double investors' money in five months with his secret robo-investing software and team of "experienced traders", in reality Alexandre pocketed most of the money. He spent $15 million of the money on his own expenses, including luxury vehicles. The small portion of funds he did invest ended up losing money.

Alexandre was sentenced to nine years in prison on July 18, 2023 and ordered to pay $249 million in forfeiture and $214 million in restitution.

Terra blockchain is halted after token crash increases threat of governance attacks

After $LUNA dropped below $0.01, Terra announced that they halted the Terra blockchain. "Terra validators have decided to halt the Terra chain to prevent governance attacks following severe $LUNA inflation and a significantly reduced cost of attack", they wrote on Twitter. This means that no transactions can continue on the Terra chain, and that holders of any tokens based on that chain (including the TerraUSD stablecoin or LUNA) can't do anything with those tokens.

Terra only announced this after halting the network, giving their users no opportunity to try to withdraw funds. They have made no announcement about whether or when they intend to bring the network back online, although it seems safe to assume that the enormous loss of confidence in Terra would make any restart short-lived.

Tether loses peg, drops below $0.95

Tether, the largest stablecoin, had a major wobble. Pegged to the U.S. dollar and widely used throughout the cryptocurrency ecosystem, even a fractional cent deviation from its peg can have enormous ramifications. Tether spent six hours below $0.99 — at one point slipping down to $0.95 — in the most significant deviation from its peg in recent history. The dip was widely connected to the recent and even more dramatic de-peg of the previously third-largest stablecoin, TerraUSD, as well as the general crypto market crash.

Tether began to recover somewhat as the day progressed, gradually returning to above $0.99. However, the de-peg has clearly shaken the cryptocurrency ecosystem. The heavy reliance on Tether means that a substantial or protracted loss of its peg would be devastating, and the open secret that Tether does not have the backing assets it once claimed has intensified fears about a possible run on Tether.

BitPrime exchange forced to pause trading due to lack of liquidity

The New Zealand cryptocurrency exchange BitPrime paused trading operations, issuing a notice to their customers: "A perfect storm has occurred, where liquidity has reduced, the market has crashed, and our overheads have increased. These have eroded trading capital and liquidity to a point where we felt we couldn't guarantee fast trading execution and liquidity of customer funds." Unlike many exchanges, BitPrime doesn't also play the role of a wallet, so customers aren't prevented from moving their crypto as they would be if this happened with an exchange that holds customer funds.

- "Important Notice For All Customers", BitPrime

CoinDesk reports that Terra's Do Kwon was behind another failed algorithmic stablecoin project

In a scoop published shortly after the catastrophes began with TerraUSD and Luna, CoinDesk reported that Terraform Labs CEO Do Kwan had also previously led a different failed stablecoin project. Using the pseudonym "Rick Sanchez", Kwon created "Basis Cash" (BAC), another algorithmic stablecoin. Basis Cash also aimed to peg to the US dollar, but never actually achieved this value. The coin has traded far below $1 for most of its existence, dropping and remaining below $0.01 in early 2021.

Do Kwon has never disclosed his involvement with this failed project. CoinDesk wrote that although their "default position is to respect the privacy of pseudonymous actors with established reputations under their well-known handles unless there is an overwhelming public interest in revealing their real-world identities", there was now "such public interest as Kwon's UST stablecoin death spirals, wreaking havoc across the broader cryptocurrency market. Amid this precarious situation, investors deserve to know that UST was not Kwon's sole attempt at making an algorithmic stablecoin work." It was not made clear in the article when CoinDesk first learned of Kwon's connection to Basis Cash, though the authors later stated they'd learned of it the night before they published.

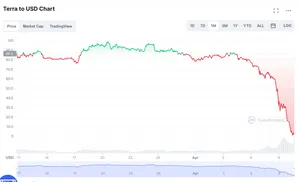

Terra $LUNA token drops in price by 98% amidst ongoing TerraUSD stablecoin collapse

Terraform Labs develops two cryptocurrencies: TerraUSD ($UST), an algorithmic stablecoin meant to be pegged to the U.S. dollar, and $LUNA, a crypto asset used both for speculation and to help maintain the UST peg. As UST dramatically lost its peg throughout early May, Luna plummeted in value alongside it. Luna was trading between $80 and $90 in the first days of May, but as of May 11 had lost 98% of its value and was hovering between $2 and $3. By midday on May 12, the token was trading at or below $0.01.

Such a dramatic crash in a cryptocurrency that was in the top ten by market cap has been devastating to some. Some members of the Terra/Luna community on Reddit have spoken of being massively over-invested in Luna, with some describing losing their life savings and appearing to be in crisis.

- Luna/USD on CoinMarketCap

- National Helpline numbers

"Cryptoqueen" Ruja Ignatova added to Europol's most wanted list in connection to OneCoin ponzi scheme

Ruja Ignatova, also known as the "Cryptoqueen", is a serial fraudster who has been on the run since 2017. In 2019, she was charged in absentia by U.S. authorities due to her connection with the OneCoin ponzi scheme.

OneCoin was a Bulgarian ponzi scheme in which investors bought packages of "tokens" with which they would supposedly "mine" cryptocurrency. Despite advertising as a decentralized cryptocurrency, OneCoin in reality was centralized on the company's servers. The scheme attracted around $4 billion in investments since its creation in 2014, and several people associated with the project have pled guilty to money laundering and fraud charges.

Coinbase adds new language regarding bankruptcy to its latest quarterly report

Coinbase added new language to its latest 10-Q, a quarterly report submitted by public companies to the SEC. In the section outlining risks to the business, Coinbase wrote: "Because custodially held crypto assets may be considered to be the property of a bankruptcy estate, in the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors."

This serves as a stark reminder to users who keep their cryptocurrency on exchanges, that although it is often a more user-friendly way to keep crypto (compared to self-custodying), it exposes users to risk like this.

Some members of the crypto community expressed shock, with Swan Bitcoin CEO Cory Klippsten tweeting, "Is this real?!?"

Former footballer Michael Owen claims his NFTs "will be the first ever that can't lose their initial value"

In what almost guarantees some fun lawsuits down the line, former footballer Michael Owen tried to hit back at "the critics" by announcing that "[his] NFTs will be the first ever that can't lose their initial value". Owen's business partner quickly turned up to do damage control, writing "we cannot guarantee or say that you cannot lose. There is always a chance".

It appeared that Owen might have meant that there would be a lower bound on resale price of the NFTs, which is neither a new concept in NFTs (see Kaiju Kongz or Rich Bulls Club), nor does it mean the NFTs "can't lose their initial value". It just means that when the NFTs do lose their initial value, collectors can't recoup even a portion of their investment.

- "Michael Owen mocked after making bold claim that his NFTs can't lose value", Manchester Evening News

G.O.A.T. token developer rug pulls for $260,000

The G.O.A.T. ("Greatest of all Tokens") project claimed to be "the new standard in cryptocurrency", with vague claims that it would "add value by addressing scalability and risk management utilizing a broad range of strategies". Unfortunately for buyers, one risk they didn't manage was that one of the project developers would suddenly sell off their holdings, making off with $260,000 while crashing the token price to nearly $0.

The remaining project developers have tried to remain positive and restore faith in the community, accusing the developer who sold of "gluttony" and "greed". The project also implemented a steep 50% tax on remaining holders to discourage them from trying to sell.

Founder of popular Azuki project admits to past rug pulls

In a blog post titled "A Builder's Journey", the founder of the popular Azuki NFT project admitted that he had also been behind the NFT projects CryptoPhunks (note the "h"), Tendies, and CryptoZunks. CryptoPhunks were simply mirrored versions of the early CryptoPunks project. In his telling, he decided to "decentralize the [CryptoPhunks] project by handing over the reins to our community". Many, if not most, others consider CryptoPhunks to be a rug pull — abandoned by its founder in a betrayal of the community. The same is true for the other two projects that Zagabond admitted he ran.

This news came as a shock to many lovers of Azuki NFTs, pricey NFTs which regularly trade for 20–30 ETH (~$45,000–$70,000). Azuki is not without its own controversies, recently facing accusations of insider trading.

- "A Builder’s Journey", by Zagabond

- Tweet by zachxbt

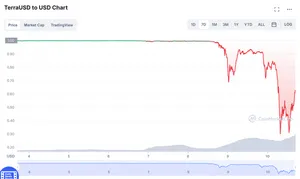

TerraUSD (UST) stablecoin dramatically loses its peg

It's been a rough few days for TerraUSD, one of several popular stablecoins pegged to the US dollar. Unlike many stablecoins like Tether or USDC, Terra is an algorithmic stablecoin, meaning that instead of (ostensibly) being backed 1-1 by various assets, they are based around an algorithm that uses various market incentives to maintain a set price. UST is the largest algorithmic stablecoin on the market at the moment, followed by projects like Fei and FRAX.

The incentives that should keep TerraUSD trading at $1 have been put to the test lately, with a combination of spiraling cryptocurrency prices across the board and some apparent large sell-offs by those holding UST. The coin dipped down to $0.992 on May 7 before some large buys returned it close to its peg. It dipped again by a smaller amount the following day, reaching a low of around $0.994. These values may seem like small changes on the micro scale, but when major stablecoins diverge from their peg by even fractions of a cent they have major effects throughout the cryptocurrency ecosystem.

On May 9, UST saw its most extreme de-peg, plunging to $0.95, then again to $0.84 later that day, despite Luna Foundation Guard liquidating $1.3 billion in Bitcoin reserves to try to restore the peg.

Do Kwon, cofounder of Terraform Labs, initially seemed to be doing his best to portray confidence on Twitter by tweeting things that give the exact opposite impression. "If yall girls are gonna fud, try to do it during my waking hours pls," he wrote on May 7. "You could listen to [crypto Twitter] influensooors about UST depegging for the 69th time. Or you could remember they're all now poor, and go for a run instead", he tweeted, somewhat blithely acknowledging UST's repeated history of losing its peg. His tweets seemed to take a more serious turn beginning the evening of May 8, as the situation grew more dire.

Attacker steals $3 million from Fortress Protocol

An attacker was able to steal 1,048 ETH (~$2.65 million) and 400,000 DAI from the Fortress Protocol borrowing and lending platform in what appears to have been an oracle manipulation attack. The attacker quickly moved their ~$3 million in stolen funds to the Tornado Cash cryptocurrency tumbler to obscure their tracks.

The exploit caused the $FTS token to drop 42%. The creators of Fortress urged people not to supply any assets to the pool as the attack was ongoing, and tweeted "we need the support of all of our partners and key organizations in the community to assist and try to freeze and bring back the funds!"

Cashera makes off with $90,000

Cashera was a project claiming to provide a "banking revolution" with its CSR crypto token. The project did many things to try to appear legitimate, including linking to government records showing a company with their name is registered in the UK and undergoing a smart contract audit by AuditRateTech. Their website boasted "partners" including VISA, PayPal, Netflix, and Spotify.

Despite all this, the project deployer suddenly minted 23 million CSR tokens, which they swapped for almost $90,000 in other assets, crashing the token value in the process by about 70%. The development team also took the project website offline.

Hunter defi project rug pulls for $1.2 million

Under the pretense of a contract upgrade, the Hunter defi project team drained the liquidity from the project, swapping the tokens for assets worth around $1.2 million. The team also took down the project website and closed the Discord server.

The rug pull was first noticed by CertiK, a blockchain security firm that had also audited the project. "We pointed out these major centralization issues in their audit," CertiK wrote on Twitter.

Fury of the Fur rug pulls for $300,000

The Fury of the Fur NFT project was a collection of 3D models that sort of resembled bears. The project advertised that the models were "metaverse and game-ready", and the roadmap promised a merchandise store, animated series, "sandbox hideout", and card game.

However, the NFT launch went poorly — fewer than 2,800 NFTs were minted out of the total supply of 9,671 NFTs. The project tried to relaunch but failed to drum up much more interest, so the creators apparently decided to call it quits — while keeping the money, of course. The project founder left a long message to the community, in which they said that they would be shutting the project and spoke at length about how difficult it had been for them.

Coinbase's new NFT marketplace hasn't had more than 200 transactions in a day since its public launch

Coinbase is a big name in the crypto exchange world, enjoying the highest trading volume in the United States. The company decided to enter the NFT trading space, first releasing an NFT marketplace to a small group of beta users, then opening it to the public on April 20.

Although the company claimed to have 3 million users on its waitlist, the public marketplace release has gone shockingly poorly given Coinbase's existing reputation. The platform has yet to see more than 200 transactions in a given day (compared to OpenSea, which regularly sees more than 100,000 transactions a day, or its smaller competitor LooksRare which sees more than 1,000 daily). Furthermore, the platform has only broken $50,000 in volume traded on five of the days it's been publicly available, with some days seeing only a few thousand dollars traded. OpenSea has been doing over $150 million in daily volume in that same time frame, and LooksRare around $100 million (though it should be noted that the prevalence of wash trading, particularly on LooksRare, makes these numbers hard to evaluate).

U.S. Treasury sanctions cryptocurrency tumbler Blender, the first sanction of its kind

The U.S. Department of the Treasury's Office of Foreign Assets Control (OFAC) announced that they had sanctioned the North Korean cryptocurrency tumbler Blender.io. This was the first U.S. government sanction levied against a cryptocurrency tumbling service. Blender was used to launder more than $20.5 million of the $620 million stolen in March from the blockchain used by the play-to-earn game Axie Infinity. The U.S. government has alleged that the North Korean state-sponsored cybercrime group Lazarus was behind the hack.

The U.S. began sanctioning various wallet addresses belonging to the hackers in mid-April, though have faced obstacles given that it is trivial for the hackers to create new wallets. The use of cryptocurrency tumblers (also called "mixers") has also stymied the government's attempts to limit the DPRK's access to the ill-gotten funds. Blender is not the primary tumbler that Lazarus has been using — that would be Tornado Cash, which they have used to tumble more than $213 million from the hack. Tornado has taken perfunctory steps to comply with sanctions, but nothing that would meaningfully impact Lazarus' ability to use the service.

- "U.S. Treasury Issues First-Ever Sanctions on a Virtual Currency Mixer, Targets DPRK Cyber Threats", U.S. Department of the Treasury

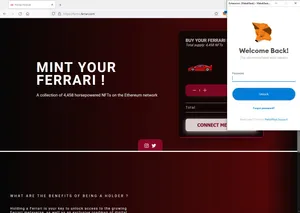

Someone hijacks a Ferrari domain to host scam NFT mint

Someone was able to gain control of a ferrari.com subdomain to create a scam NFT mint. Most scam NFT projects rely on eager NFT collectors not noticing a URL that isn't quite right — for example, something like ferrari-nft.com. This one was able to gain some additional legitimacy by using an actual ferrari.com subdomain. Additionally, Ferrari had recently announced an upcoming NFT project, making the scam project seem more plausible.

Sadly for the scammer, the scam was discovered and shut down when they had only managed to scam one person. The unsuspecting collector sent 0.3 ETH ($800), which the scammer transferred to Tornado Cash.

- "Ferrari subdomain hijacked to push fake Ferrari NFT collection", BleepingComputer

Day of Defeat project rug pulls for $1.35 million

The token associated with the Day of Defeat project, which describes itself as a "radical social experiment token mathematically designed to give holders 10,000,000X PRICE INCREASE" (🚩🚩🚩), suddenly dropped in value by more than 96% as the project rug pulled. More than $1.35 million worth of assets were drained from the BSC-based project and transferred to external wallets.

The project's website is one of the most absurd I've seen, promising that "all final holders will get 10,000,000x gains". Their project roadmap includes a "mystery plan" that results in a 1,000,000x price increase. Their FAQ states, "First of all, we promise that the team will not redeem the fund pool." Apparently projects based on pinky swears aren't great investments.

After the funds were drained, the project claimed that they had been compromised by an external actor, and had "reported to Binance and local authorities".

OpenSea Discord hacked

The OpenSea Discord server was compromised, allowing a scammer to post a seemingly-official announcement that OpenSea was partnering with YouTube on a line of NFTs. They urged people to act quickly to snag one of only 100 free NFTs that would offer "insane utility".

Given OpenSea's prominence, it's surprising that the hacker managed to obtain relatively few NFTs of much value. The wallet appeared to have successfully stolen only 13 NFTs, none of which were from high-value collections, that are worth a collective $20,000 if resold at the collections' floor prices.

OpenSea tweeted several messages acknowledging the hack and urging users not to click any links. They have not yet confirmed that they've conclusively re-secured their server.

"Double your money" scam using an old livestream of Elon Musk, Jack Dorsey, and Cathie Wood earns crypto scammers $1.3 million in 24 hours

Crypto scammers on YouTube rehosted a "live" panel discussion — actually from "The ₿ Word" conference in July 2021 — in which Elon Musk, Jack Dorsey, and Cathie Wood discussed "Bitcoin as a Tool for Economic Empowerment". The scammers added a frame around the video that advertised "giveaways" and "double your money" scam websites. The websites promised that if you sent cryptocurrency to the address, you would receive twice as much in return — a classic scam I remember from the Runescape days, which has also enjoyed success in crypto markets for years. The scammers inflated YouTube subscriber and active watcher numbers to add legitimacy to their streams, and some of them faked screenshots of tweets from Musk.

McAfee identified 26 scam websites that were linked from the YouTube livestreams, which altogether took in $1.3 million in Bitcoin and Ether in a 24 hour period.

Mining Capital Coin CEO indicted for $62 million investment fraud scheme

The Department of Justice unsealed an indictment on May 5, showing that Mining Capital Coin's CEO and founder Luiz Capuci Jr. was charged with orchestrating a $62 million investment fraud. Capuci allegedly misled investors about MCC's program, which he said would use investors' money to mine new cryptocurrency and would generate guaranteed returns. Instead, Capuci put the funds into his own crypto wallets, and used them to fund his own lifestyle of Lamborghinis, real estate, and a yacht. Capuci also allegedly ran a pyramid scheme of promoters, to whom he promised luxury gifts including iPads and luxury cars.

Capuci was charged with conspiracy to commit wire fraud, conspiracy to commit securities fraud, and conspiracy to commit international money laundering. If convicted on all counts, he could be sentenced to up to 45 years in prison.

- "CEO of Mining Capital Coin Indicted in $62 Million Cryptocurrency Fraud Scheme", U.S. Department of Justice

Pragma defi protocol developers rug pull for $1.5 million

The Pragma defi project on the Fantom blockchain announced that their treasury and project wallets had been drained for around $1.5 million in $FTM.

The rug pull appeared to have been perpetrated by one team member, although several other team members had to sign off on the transaction in order for it to go through.

The team had had their real-life identities verified by Obsidian, and remaining team members said they were working with Obsidian to try to investigate those behind the theft. Third-party KYC verification like the service Obsidian provides is often used by crypto projects to increase trust, though Pragma is hardly the first project with this kind of verification that stole funds anyway.

Juno accidentally transfers $36 million in seized funds to inaccessible wallet address

A protracted discussion and two different votes ended with the Juno project deciding to confiscate all but 50,000 of the 3 million $JUNO accumulated by one individual. When the discussions began, the 2.95 million $JUNO to be confiscated were worth a combined $121 million. However, the $JUNO price has dropped from the then all-time-high of around $40 to under $13, putting the value of the tokens to be confiscated closer to $38 million.

Juno intended to transfer the seized tokens from the individual whale's wallet to a community-controlled wallet. However, the person making the transfer accidentally copied and pasted the wrong value, resulting in the funds being sent to a wallet address that no one can access — effectively burning the tokens.

Daniel Hwang, who helps run one of the Juno validators, said to CoinDesk, "We fucked up big time". He also offered an unusual opinion: "Validators should have due diligenced for ourselves to actually check the code we're executing and running".

Shortly after the botched transaction, the Juno community began voting on a proposal to hard fork a second time to fix their mistake.

Attacker compromises MM.Finance to redirect $2 million in crypto assets to their own wallet

MM.Finance, a group of crypto projects based on the Cronos blockchain, suffered an attack that allowed a hacker to redirect more than $2 million worth of crypto assets that were being exchanged through the project's website to their own wallet. Although MM.Finance described the attack as "DNS hijacking", it seems unlikely this is an accurate description of the attack, which seems more likely to involve phished credentials to their domain service providers.

"Please do not perform any transactions or your funds will be sent to the exploiter wallet," MM.Finance tweeted shortly before taking the website offline. Three days earlier, MM.Finance had published a blog post to address "FUD" in their ecosystem stemming from a popular Reddit post that described MMF as an "inverse pyramid of derivatives" that the author believed would "topple", and outlined the project's "rosy future".

The project promised to try to compensate users, with its developers foregoing 45 days of trading fees to reimburse users. They also appealed to the OKC crypto exchange to intervene to help recover funds from someone they believed to be the attacker, and threatened the attacker with the FBI. "With all these information, we have more than what we need to bring this information to the FBI," they wrote on Twitter. "So here's the deal, return 90% of the funds you stole and we will let this go, no questions asked. You have 48 hours to return these funds."

- Tweet by MM.Finance

- "Mm Finance — The road ahead", MM.Finance blog

- "Personal Take on Events and Existing Tokenomics", post from r/MMFinance

- "DNS Hi-Jacking Post Mortem & Compensation", MM.Finance blog

ape holders can use multiple slurp juices on a single ape

a lotta yall still dont get it

ape holders can use multiple slurp juices on a single ape

so if you have 1 astro ape and 3 slurp juices you can create 3 new apes

Tonight's slurp juice mint event is essentially a minting event for both Lab Monkes and Special Forces

Video game company Square Enix agrees to sell much of their Western IP so they can go into the blockchain market

Video game company Square Enix, the creators of titles including Deus Ex and Tomb Raider, agreed to sell off the intellectual property rights to those games, as well as other games and their respective game studios. The move, they said, was so they could invest more heavily in "blockchain, AI, and the cloud". This didn't come as an enormous surprise, as in January, Square Enix CEO announced these intentions in a letter that acknowledged that that (apparent subset) of players who "play to have fun" wouldn't be thrilled with their blockchain plans.

The sale agreement announcement came at a tough time for Square Enix, as it was published the same day as a report from the Wall Street Journal that "NFT Sales are Flatlining".