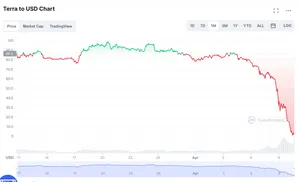

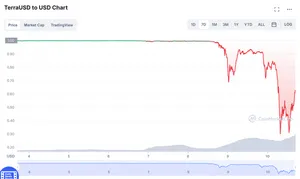

It's been a rough few days for TerraUSD, one of several popular stablecoins pegged to the US dollar. Unlike many stablecoins like Tether or USDC, Terra is an algorithmic stablecoin, meaning that instead of (ostensibly) being backed 1-1 by various assets, they are based around an algorithm that uses various market incentives to maintain a set price. UST is the largest algorithmic stablecoin on the market at the moment, followed by projects like Fei and FRAX.The incentives that should keep TerraUSD trading at $1 have been put to the test lately, with a combination of spiraling cryptocurrency prices across the board and some apparent large sell-offs by those holding UST. The coin dipped down to $0.992 on May 7 before some large buys returned it close to its peg. It dipped again by a smaller amount the following day, reaching a low of around $0.994. These values may seem like small changes on the micro scale, but when major stablecoins diverge from their peg by even fractions of a cent they have major effects throughout the cryptocurrency ecosystem.

On May 9, UST saw its most extreme de-peg, plunging to $0.95, then again to $0.84 later that day, despite Luna Foundation Guard liquidating $1.3 billion in Bitcoin reserves to try to restore the peg.

Do Kwon, cofounder of Terraform Labs, initially seemed to be doing his best to portray confidence on Twitter by tweeting things that give the exact opposite impression. "If yall girls are gonna fud, try to do it during my waking hours pls," he wrote on May 7. "You could listen to [crypto Twitter] influensooors about UST depegging for the 69th time. Or you could remember they're all now poor, and go for a run instead", he tweeted, somewhat blithely acknowledging UST's repeated history of losing its peg. His tweets seemed to take a more serious turn beginning the evening of May 8, as the situation grew more dire.