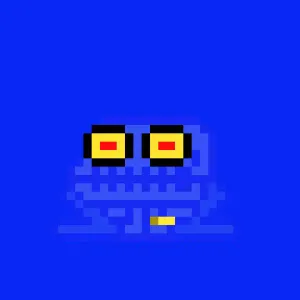

It's hard to say why the collector accepted such a low offer. Some have speculated that they were tax loss harvesting to offset other gains, while others have wondered if the collector's account might have been compromised. It's also possible that the collector was cutting losses, not expecting the demand for their NFT to rebound anytime soon.

NFT collector sells pixel art toad at a $1 million loss

In October 2021, an NFT collector dropped 300 ETH (then $1.05 million) on CrypToadz #2155, a pixel art image of a blue toad skeleton on a blue background. On June 13, they sold the NFT for 6.9 ETH (~$8,300), a $1.02 million loss.

Tron's algorithmic stablecoin (USDD) wobbles

USDD, the algorithmic stablecoin belonging to the Tron network, dipped as low as $0.91 from its $1 peg on June 13 amidst a day of turmoil elsewhere in the crypto ecosystem. Blockchain analytics firm Nansen observed that Oapital, one of the funds that successfully profited off the Terra de-peg, had started to move large amounts of USDD (as well as other stablecoins). "Doesn't look great", Nansen tweeted.

Tron founder Justin Sun tweeted that the Tron DAO would deploy $2 billion (with a B) in capital to fight short sellers, writing: "Short squeeze is coming".

Crypto.com and BlockFi announce layoffs

On June 10, Crypto.com announced they would be "making targeted reductions" of 260 people, amounting to around 5% of their workforce. On June 13, BlockFi announced that they were in "the gut wrenching position of needing to reduce our headcount" by around 20%. BlockFi has around 850 staff, suggesting they plan to lay off 170 people.

These announcements followed a June 2 layoff announcement by Gemini and the announcement by Coinbase that same day that they would be rescinding already-accepted job offers.

Rumors of a downturn across the tech industry more broadly have been swirling for several months, but crypto companies appear to be being hit particularly hard as they simultaneously endure "crypto winter".

- "Crypto crash wreaking havoc on DeFi protocols, CEXs", Cointelegraph

Binance pauses Bitcoin withdrawals for 3 hours due to "stuck" transactions

Binance paused Bitcoin withdrawals for three hours on June 13, explaining that some network maintenance resulted in transactions becoming "stuck and not able to be processed successfully". Although founder and CEO Changpeng Zhao predicted the pause would only take thirty minutes, the issue took closer to three hours to resolve.

I love it when I go to my bank to grab some cash from the ATM and discover that I can't, because someone else's cash clogged up the pipe.

The pause occurred as Bitcoin was reaching record low prices not seen since 2020, contributing to the ongoing pattern of Binance suddenly pausing withdrawals or undergoing maintenance during periods of chaos in the crypto ecosystem.

Terra investors file class action lawsuit against Binance.US

A group of people who put money into Terra (UST), the stablecoin that collapsed in May, have filed a class action lawsuit against Binance.US. Binance.US is a crypto exchange that operates within the US, managed independently from Binance, which is not available to US customers due to fears that it would run afoul of US securities regulations.

The lawsuit argues that UST is an unregistered security, and that as a result, Binance.US was violating securities laws by listing it. The lawsuit also alleges that Binance.US misled investors, leading them to believe that UST was more stable than it actually was. More than 2,000 investors have joined the lawsuit.

"SeaFlower" hacks target crypto users via backdoored iOS and Android crypto wallets

The Confiant security research group has discovered a group that is backdooring and distributing versions of legitimate crypto wallets including Coinbase Wallet, MetaMask, TokenPocket, and imToken. The hackers have created reverse-engineered versions of the crypto wallets that operate as designed, but also steal the user's seed phrase, later using it to drain the users' cryptocurrency.

The attackers have distributed the tampered applications through websites that clone the legitimate applications' websites. Through search engine poisoning, primarily via Chinese search engines like Baidu, the attackers have successfully gotten unsuspecting users to install the malicious programs.

- "Hackers clone Coinbase, MetaMask mobile wallets to steal your crypto", BleepingComputer

Lido-staked Ether (stETH) loses peg

Lido-staked ETH, a project that offers to allow users to stake ETH for the purposes of securing it after the Ethereum "merge" — that is, the ever-delayed move to proof-of-stake. Although stETH is backed 1:1 with ETH, it's not very liquid aside from the primary liquidity on Curve. Huge sell-offs of stETH for ETH have been causing slippage in the Curve pool, which was off peg by around 5% and heavily imbalanced on June 12.

Crypto researcher Small Cap Scientist suggested on June 9 that the sell-offs may have been triggered by a "canary in the coal mine": a 50,000 stETH (nominally worth $45.8 million) sell-off by Alameda Research, a trading firm founded by Sam Bankman-Fried. SCS also reported that Celsius Network was "quickly running out of liquid funds to pay back their investors", and "they are taking massive loans" against "billions in illiquid positions" to pay back customers.

Celsius pauses all withdrawals

The Celsius platform announced that they would be pausing all withdrawals, swaps, and transfers due to "extreme market conditions".

There has been a lot of concern lately about Celsius' reserves and its ability to honor redemptions, with some speculating that the platform might be underwater and forced to default. Celsius released a blog post on June 7 titled, "Damn the Torpedoes, Full Speed Ahead" where they accused "vocal actors" of "spreading misinformation and confusion", and promised that "Celsius continues to process withdrawals without delay", and that "Celsius has the reserves (and more than enough ETH) to meet obligations".

Celsius' June 12 announcement did not include any details on what their plans would be, just that they hoped it would allow them to "stabilize liquidity and operations while we take steps to preserve and protect assets".

On June 14, the Wall Street Journal reported that Celsius had hired restructuring attorneys.

Offline Cash project finally gives the world what it really needs: physical digital physical cash

Some crypto advocates have long promoted crypto as a proper digital equivalent to cash. Physical dollars have a lot of benefits, including that you don't need a bank account to use them and they provide a lot of privacy. Although bank transfers and apps like Venmo offer digital ways to transfer money, they typically require a bank account to use, and they leave a digital record of the transaction. Crypto advocates have long promised that crypto is a proper digital equivalent to cash, despite its own accessibility and privacy concerns.

Anyway, a project called Offline Cash has sprung up. In a stunning example of Poe's Law, the project seeks to provide a physical form of that digital physical cash people have spent so much time working on.

Hear me out: imagine you had paper notes that you could transfer to people in lieu of making a Bitcoin transaction! And unlike regular cash, it has an expiration date to keep track of!

Scammers compromise verified, 5-million-follower Twitter account for Venezuelan newspaper El Universal, use it to promote fake Goblintown site

Scammers successfully compromised the Twitter account for El Universal, a Venezuelan newspaper. The account is verified, and has five million followers. The scammers used the account to promote "goblintowm" (note the m on the end), a fake website pretending to be the recently-popular Goblintown project. Users who connected their wallets to try to mint the free NFTs instead saw their wallets drained of their cryptocurrency and NFTs.

One of the wallets used by the scammers had stolen 64 NFTs, though most of them were low in value. The address had also pulled in 16.5 ETH (~$30,000). However, most scammers rotate wallets, and this likely doesn't reflect the total damage from the scam.

- Tweet by NFTherder

- Archived copy of the compromised Twitter account